Coordinating Processing Networks with Automated Charge Frameworks to Handle Client Billing Cycles in Portable Commerce Setups

Portable commerce setups rely on seamless coordination between processing networks and automated charge frameworks to manage recurring client billing cycles without manual intervention at each step. These systems connect merchant accounts directly to client payment methods through standardized protocols that trigger charges on predetermined schedules whether daily, weekly, or monthly. Observers note that this integration reduces delays in revenue collection while maintaining accurate records across multiple transactions.

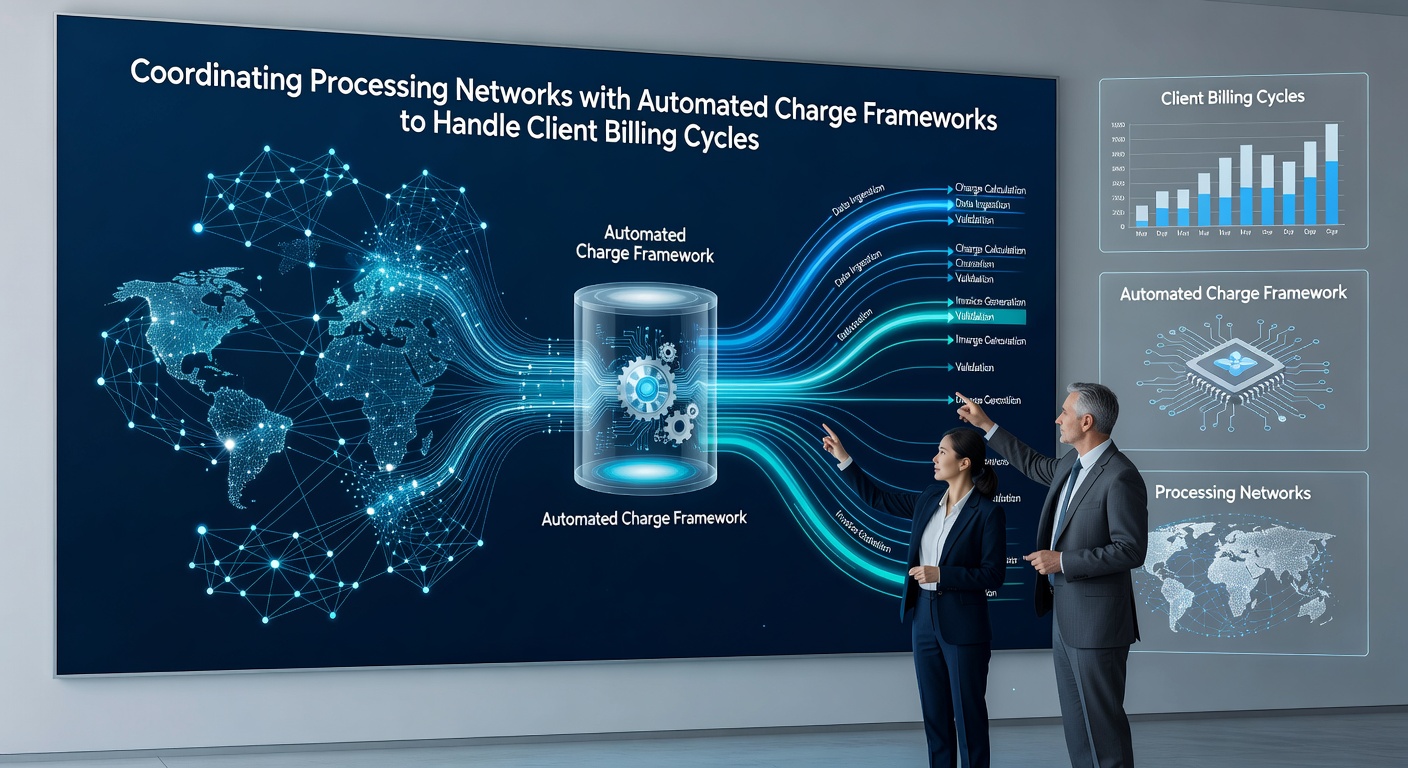

Core Components of Network Coordination

Processing networks serve as the backbone that routes authorization requests from mobile devices to acquiring banks and card networks. Automated charge frameworks overlay these networks by storing billing parameters such as cycle dates, amounts, and retry logic in centralized ledgers that activate when conditions align. Data from industry reports shows that businesses handling high volumes of subscriptions achieve settlement rates above 95 percent when these two layers operate in tandem rather than through separate manual processes.

Technicians configure the frameworks to poll processing networks at regular intervals for status updates on pending charges. This polling mechanism allows frameworks to adjust billing cycles dynamically if network responses indicate temporary holds or declines. Researchers at institutions studying digital payments have documented cases where such adjustments prevent cascading failures across thousands of client accounts during peak mobile usage periods.

Automation in Billing Cycle Management

Automated frameworks execute predefined rules for each billing cycle by pulling client data from secure databases and submitting charge requests through established processing channels. In portable commerce the frameworks account for device-specific variables such as connectivity fluctuations and session timeouts that can interrupt standard flows. Evidence suggests that frameworks incorporating real-time network feedback loops complete cycles with fewer interruptions compared to static scheduling approaches.

One study revealed that organizations deploying these coordinated systems in mobile environments processed over 2 million recurring transactions monthly with error rates below 2 percent. The frameworks handle proration for mid-cycle changes, apply taxes based on client location, and generate notifications automatically once charges clear through the processing network.

Implementation in Mobile Commerce Environments

Mobile commerce platforms integrate these coordinated systems through backend services that communicate with both the processing networks and the charge frameworks simultaneously. Developers set up event listeners within the frameworks that respond to network confirmations by updating client ledgers and advancing the next billing date. This event-driven approach ensures that billing cycles remain synchronized even when clients switch devices or update payment credentials mid-cycle.

Take one logistics company that shifted its mobile invoicing operations to coordinated frameworks in early 2025. The transition allowed the firm to align weekly client charges with network settlement windows, resulting in improved cash flow predictability according to internal metrics shared with payment consultants. Frameworks also incorporate retry schedules that space out attempts across different processing network nodes to avoid rate limits imposed by card issuers.

Regulatory Alignment and Reporting

Coordination efforts must align with regional payment regulations that govern how automated charges interact with client accounts. The European Central Bank maintains guidelines on payment service providers that require transparent cycle management and dispute resolution pathways built into automated frameworks. European Central Bank payment frameworks emphasize audit trails that link each network authorization to the corresponding billing cycle entry.

In Australia the Reserve Bank has outlined expectations for recurring payment transparency that affect how frameworks document consent and schedule changes. Reserve Bank of Australia payment system resources highlight the need for frameworks to retain records that processing networks can reference during reconciliation. Updates scheduled for June 2026 will introduce enhanced reporting fields for cross-border mobile transactions that frameworks must accommodate through network coordination layers.

Operational Challenges and Solutions

Network latency in portable environments can disrupt automated charge timing especially when frameworks attempt to execute cycles during high-traffic periods. Solutions involve distributing charge requests across multiple network endpoints and setting staggered execution windows within the frameworks. Those who've studied operational data find that these distribution methods maintain cycle completion rates above 98 percent even under variable mobile network conditions.

Frameworks also manage partial payments and overages by triggering follow-up charges or credits through the same processing pathways. This capability proves essential for commerce setups that bill based on usage metrics captured from mobile applications. Observers note that accurate metering combined with automated coordination minimizes discrepancies that otherwise require manual intervention.

Conclusion

Coordinating processing networks with automated charge frameworks establishes reliable handling of client billing cycles in portable commerce setups through synchronized data flows and event responses. Organizations that implement these connections report consistent cycle execution and reduced administrative overhead. As regulatory expectations evolve in 2026 the frameworks will continue to adapt their network interfaces to maintain compliance while supporting mobile transaction volumes.